The goal of the bate package is to present some

functions to compute quantiles of the empirical distribution of the

bias-adjusted treatment effect (BATE) in a linear econometric model with

omitted variables. To analyze such models, a researcher should consider

four regression models: (a) a short regression model where the outcome

variable is regressed on the treatment variable, with or without

additional controls; (b) an intermediate regression model where

additional control variables are added to the short regression; (c) a

hypothetical long regression model, where an index of the

omitted variable(s) is added to the intermediate regressions; and (d) an

auxiliary regression where the treatment variable is regressed on all

observed (and included) control variables.

As an example, suppose a researcher has estimated the following model, y = α + β1x + γ1w1 + γ2w2 + ε , and is interested in understanding the impact of some omitted variables on the results. In this case:

The treatment effect is β1, but in the presence of omitted variables, this will be estimated with a bias. The functions in this package will allow a researcher to create quantiles of the empirical distribution of the BATE, i.e. the treatment effect once we have adjusted for the effect of omitted variable bias.

The researcher will need to supply the data set (as a data frame), the name of the outcome variable, the name of the treatment variable, and the names of the additional regressors in the intermediate regression. The functions in this package will then compute the quantiles of the empirical distribution of BATE.

Two parameters capture the effect of the omitted variables in this set up.

The first parameter is δ. This captures the relative

strength of the unobservables, compared to the observable controls, in

explaining variation in the treatement variable. In the

functions below this is denoted as the parameter delta.

This parameter is a real number and can take any value on the real line,

i.e. it is unbounded. Hence, in any specific analysis, the researcher

will have to choose a lower and an upper bound for delta.

For instance, if in any empirical analysis, the researcher believes,

based on knowledge of the specific problem being investigated, that the

unobservables are less important than the observed controls in

explaining the variation in the treatment variable, then she

could choose delta to lie between 0 and 1. On the other

hand, if she believes that the unobservables are more important

than the observed controls in explaining the variation in the

treatment variable, then she should choose delta

to lie between 1 and 2 or 1 and 5.

The second parameter is

Rmax. This captures the

relative strength of the unobservables, compared to the observable

controls, in explaining variation in the outcome variable. In

the functions below, this is captured by the parameter

Rmax. The parameter Rmax is the R-squared in

the hypothetical long regression. Hence, it lies between the R-squared

in the intermediate regression (R̃) and 1. Since the lower bound

of Rmax is given by R̃, in any specific analysis,

the researcher will only have to choose an upper bound for

Rmax.

In a specific empirical analysis, a researcher will use domain

knowledge about the specific issue under investigation to determine a

plausible range for delta (e.g. 0.01 ≤ δ ≤ 0.99).

This will be given by the interval on the real line lying between

deltalow and deltahigh (the researcher will

choose deltalow and deltahigh). Using the

example in this paragraph, deltalow=0.01 and

deltahigh=0.99.

In a similar manner, a researcher will use domain knowledge about the

specific issue under investigation to determine Rmax. Here,

it will be important to keep in mind that Rmax is the

R-squared in the hypothetical long regression. Now, it is unlikely that

including all omitted variables and thereby estimating the hypothetical

long regression will give an R-squared of 1. This is because, even after

all the regressors have been included, some variation of the outcome

might be plausibly explained by a stochastic element. Hence,

Rmax will most likely be different from, and less than, 1.

This will be denoted by Rhigh

(e.g. Rmax=0.61).

How is the omitted variable bias and the BATE computed? The key

result that is used to compute the BATE is this: the omitted variable

bias is the real root of a cubic equation whose coefficients

are functions of the parameters of the short, intermediate and auxiliary

regressions and the values of delta and Rmax.

In a specific empirical analysis, the parameters of the short,

intermediate and auxiliary regressions are known. Hence, the

coefficients of the cubic equation become functions of

delta and Rmax, the two key parameters that

the researcher chooses, using domain knowledge.

Once the researchers has chosen deltalow,

deltahigh and Rhigh, this defines a bounded

box on the (delta, Rmax) plane defined by the

Cartesian product of the interval [deltalow,

deltahigh] and of the interval [Rlow,

Rhigh]. The main functions in this package computes the

root of the cubic equation on a sufficiently granular grid (the degree

of granularity will be chosen by the user) covering the bounded box.

To compute the root of the cubic equation, the algorithm first evaluates the discriminant of the cubic equation on each point of the grid and partitions the box into two regions: (a) unique real root (URR) and NURR (no unique real root). There are three cases to consider.

delta direction to generate a nonempty intersection

with a URR region. Once that is found, the algorithm implements the

steps outlined in step 2.The bias is then used to compute the BATE, which is defined as the estimated treatment effect in the intermediate regression minus the bias. This will generate an empirical distribution of the BATE. Asymptotic theory shows that the BATE converges in probability to the true treatment effect. Hence, the interval defined by the 2.5-th and 97.5-th quantiles of the empirical distribution of the BATE will contain the true treatment effect with 95 percent probability.

An useful function to collect relevant parameters from the short, intermediate and auxiliary regressions is:

collect_par(): collects parameters from the short,

intermediate and auxiliary regressions; (user provides name of the data

set, name of outcome variable, name of treatment variable, names of

control variables in the short regression, if relevant, and names of

additional variables in the intermediate regression); the output of this

function is a data frame.Users can use the output from collect_par() to construct

an area plot of the bounded box using:

urrplot(): creates a colored area plot of the bounded

box chosen by the user demarcating the area where the cubic equation has

unique real root (URR) from the area where the cubic equation has three

real roots (NURR); the output is a plot object.The main functions in this package that are available for users to compute empirical distributions of omitted variable bias and BATE are:

ovbias(): computes the empirical distribution of

omitted variable bias and BATE (takes the output from

collect_par() as one of the inputs); the output of this

function is a list;ovbias_par(): computes the empirical distribution of

omitted variable bias and BATE (takes the data frame, name of outcome

variable, name of treatment variable, names of control variables in the

short regression, if relevant, and names of additional variables in the

intermediate regression, as inputs); the output of this function is a

list;ovbias_lm(): computes the empirical distribution of

omitted variable bias and BATE (takes three lm objects

corresponding to the short, intermediate and auxiliary regressions as

inputs); the output of this function is a list.Using the output from ovbias(),

ovbias_par() or ovbias_lm(), users can

construct various plots:

cplotbias(): contour plot of the bias over the bounded

box; the output of this function is a plot object;dplotbate(): histogram and density plot of BATE; the

output of this function is a plot object;The methodology proposed in Oster (2019) is implemented via these functions:

osterbds(): identified sets according to Oster’s

methodology; the output of this function is a data frame;osterdelstar(): the value of δ* for

a chosen value of Rmax;

the output of this function is a data frame;delfplot(): a plot of the graph of the function,

δ = f(Rmax);

the output of this function is a plot object.You can install the development version of bate from GitHub with:

# install.packages("devtools")

devtools::install_github("dbasu-umass/bate")Let us load the data set.

data("NLSY_IQ")The data set has two .RData objects:

NLSY_IQ (to be used for the analysis of maternal behavior

on child IQ) and NLSY_BW (to be used for the analysis of

maternal behavior on child birthweight).

Let us see the names of the variables in the NLSY_IQ

data set.

names(NLSY_IQ)

#> [1] "iq_std" "BF_months" "mom_drink_preg_all"

#> [4] "lbw_preterm" "age" "female"

#> [7] "black" "motherAge" "motherEDU"

#> [10] "mom_married" "income" "sex"

#> [13] "race"Let us set age and race as factor

variables

NLSY_IQ$age <- factor(NLSY_IQ$age)

NLSY_IQ$race <- factor(NLSY_IQ$race)Let us work with the following example:

iq_std ~ BF_months + sex + ageiq_std ~ BF_months + sex + age + income + motherAge + motherEDU + mom_married + race.Let us use the collect_par() function to collect

parameters from the short, intermediate and auxiliary regressions. Note

how other_parameters is a subset of control.

The researcher needs to make sure that control includes the

names of all regressors in the intermediate regression, other

than the treatment variable.

parameters <- bate::collect_par(data=NLSY_IQ,

outcome="iq_std",

treatment="BF_months",

control=c("age","sex","income","motherAge","motherEDU","mom_married","race"),

other_regressors = c("sex","age"))Let us see the parameters.

(parameters)

#> beta0 R0 betatilde Rtilde sigmay sigmax taux

#> BF_months 0.04447926 0.04465201 0.01740748 0.255621 0.9900242 4.629618 18.99883Let us choose the dimensions of the bounded box over which we want the bias computation to be carried out.

# Upper bound of Rmax

Rhigh <- 0.61

# Lower bound of delta

deltalow <- 0.01

# Upper bound of delta

deltahigh <- 0.99

# step size to construct grid

e <- 0.01Now we can use the ovbias() function to compute the

empirical distribution of omitted variable bias and BATE. Note that this

step make take a few minutes, depending on the dimensions of the box and

the size of e, to complete itself.

OVB <- bate::ovbias(

parameters = parameters,

deltalow=deltalow,

deltahigh=deltahigh,

Rhigh=Rhigh,

e=e)We can now see the quantiles of omitted variable bias

(OVB$bias_Distribution)

#> 2.5% 5% 50% 95% 97.5%

#> 0.000 0.000 0.009 0.034 0.039and quantiles of the BATE (computed over the bounded box we chose above).

(OVB$bstar_Distribution)

#> 2.5% 5% 50% 95% 97.5%

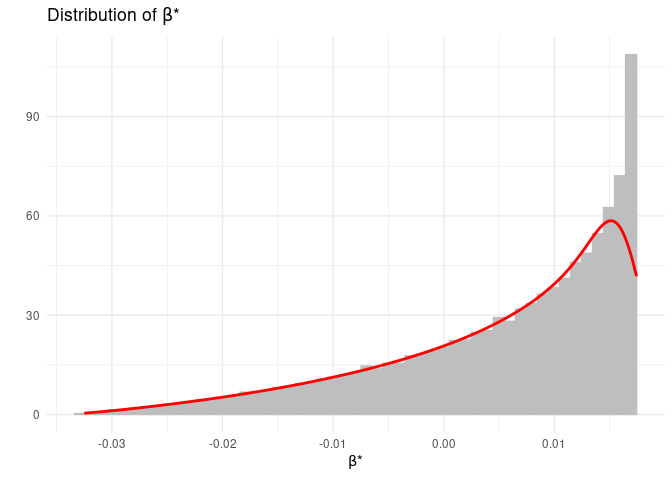

#> -0.021 -0.017 0.009 0.017 0.017We can create the histogram and density plot of the omitted variable bias.

bate::dplotbate(OVB$Data)

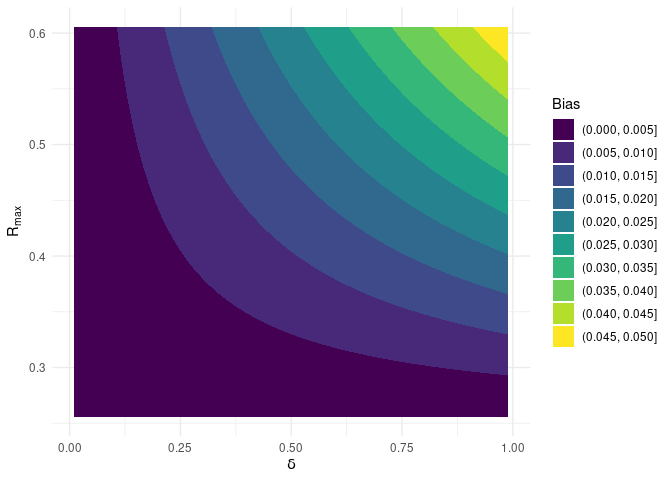

We can also create a contour plot of BATE over the bounded box.

bate::cplotbias(OVB$Data)