The Time Series Modeling Companion to healthyR

To view the full wiki, click here: Full healthyR.ts Wiki

healthyR.ts is a comprehensive R package designed

specifically for time series analysis and forecasting of hospital

administrative and clinical data. Built on the powerful tidymodels ecosystem, it provides

a consistent, user-friendly framework that simplifies complex time

series workflows.

Hospital data analysis often requires handling time series for metrics like: - Average Length of Stay (ALOS) - Readmission rates - Patient volumes and admissions - Bed occupancy rates - Clinical outcomes over time

healthyR.ts takes the guesswork out of time series

analysis by providing:

✅ Automated Workflows - One-function solutions for

complete modeling pipelines

✅ Visual Analytics - Rich plotting functions for data

exploration

✅ Data Generators - Simulate realistic time series for

testing and validation

✅ Statistical Tools - Comprehensive suite of time

series statistics

✅ Clustering - Feature-based time series clustering

capabilities

✅ Forecasting - 15 automated model workflows (ARIMA,

Prophet, XGBoost, and more)

Complete end-to-end modeling pipelines in a single function call:

Each function handles recipe creation, model specification, workflow setup, model fitting, tuning, and calibration automatically.

Generate synthetic time series data for testing: - Random walks and Brownian motion - Geometric Brownian motion - ARIMA simulations - Custom parameter configurations

Install the latest stable version from CRAN:

install.packages("healthyR.ts")Get the latest features and bug fixes from GitHub:

# install.packages("devtools")

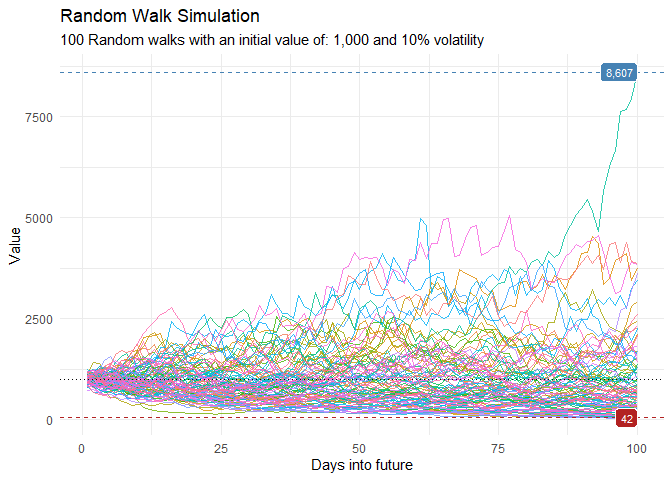

devtools::install_github("spsanderson/healthyR.ts")Generate and visualize random walk data to understand market volatility or patient flow variations:

library(healthyR.ts)

library(ggplot2)

df <- ts_random_walk()

head(df)

#> # A tibble: 6 × 4

#> run x y cum_y

#> <dbl> <dbl> <dbl> <dbl>

#> 1 1 1 0.113 1113.

#> 2 1 2 0.119 1245.

#> 3 1 3 -0.0178 1223.

#> 4 1 4 0.141 1396.

#> 5 1 5 -0.163 1169.

#> 6 1 6 -0.0485 1112.Now that the data has been generated, lets take a look at it.

df %>%

ggplot(

mapping = aes(

x = x

, y = cum_y

, color = factor(run)

, group = factor(run)

)

) +

geom_line(alpha = 0.8) +

ts_random_walk_ggplot_layers(df)

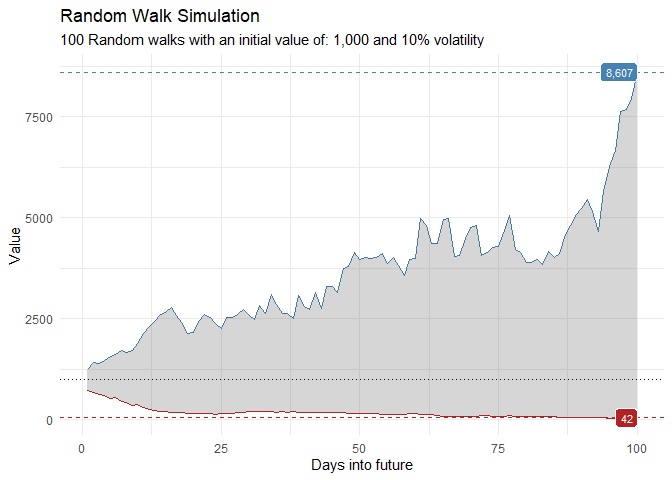

That is still pretty noisy, so lets see this in a different way. Lets clear this up a bit to make it easier to see the full range of the possible volatility of the random walks.

library(dplyr)

library(ggplot2)

df %>%

group_by(x) %>%

summarise(

min_y = min(cum_y),

max_y = max(cum_y)

) %>%

ggplot(

aes(x = x)

) +

geom_line(aes(y = max_y), color = "steelblue") +

geom_line(aes(y = min_y), color = "firebrick") +

geom_ribbon(aes(ymin = min_y, ymax = max_y), alpha = 0.2) +

ts_random_walk_ggplot_layers(df)

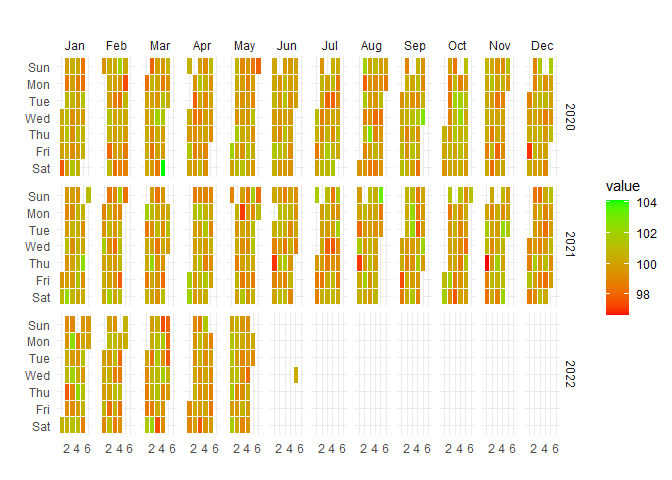

Visualize temporal patterns in your data with calendar heatmaps - perfect for identifying seasonal trends or unusual patterns in hospital metrics:

data_tbl <- data.frame(

date_col = seq.Date(

from = as.Date("2020-01-01"),

to = as.Date("2022-06-01"),

length.out = 365*2 + 180

),

value = rnorm(365*2+180, mean = 100)

)

ts_calendar_heatmap_plot(

.data = data_tbl

, .date_col = date_col

, .value_col = value

, .interactive = FALSE

)

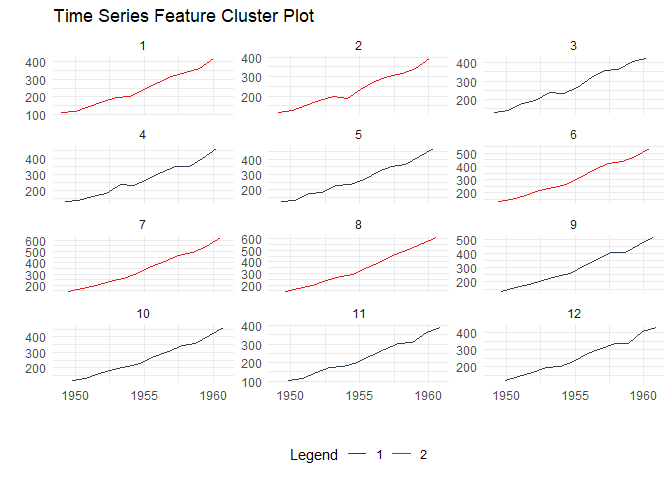

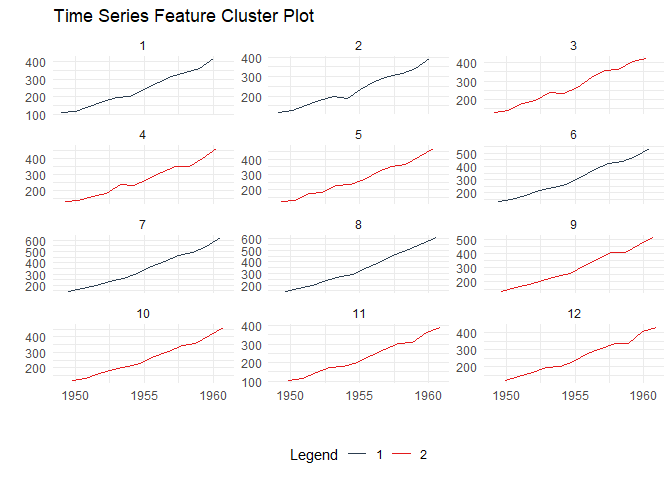

Discover patterns by clustering time series based on their statistical features:

data_tbl <- ts_to_tbl(AirPassengers) %>%

mutate(group_id = rep(1:12, 12))

output <- ts_feature_cluster(

.data = data_tbl,

.date_col = date_col,

.value_col = value,

group_id,

.features = c("acf_features","entropy"),

.scale = TRUE,

.prefix = "ts_",

.centers = 3

)

ts_feature_cluster_plot(

.data = output,

.date_col = date_col,

.value_col = value,

.center = 2,

group_id

)

#> $plot

#> $plot$static_plot

#>

#> $plot$plotly_plot

#>

#>

#> $data

#> $data$original_data

#> # A tibble: 144 × 4

#> index date_col value group_id

#> <yearmon> <date> <dbl> <int>

#> 1 Jan 1949 1949-01-01 112 1

#> 2 Feb 1949 1949-02-01 118 2

#> 3 Mar 1949 1949-03-01 132 3

#> 4 Apr 1949 1949-04-01 129 4

#> 5 May 1949 1949-05-01 121 5

#> 6 Jun 1949 1949-06-01 135 6

#> 7 Jul 1949 1949-07-01 148 7

#> 8 Aug 1949 1949-08-01 148 8

#> 9 Sep 1949 1949-09-01 136 9

#> 10 Oct 1949 1949-10-01 119 10

#> # ℹ 134 more rows

#>

#> $data$kmm_data_tbl

#> # A tibble: 3 × 3

#> centers k_means glance

#> <int> <list> <list>

#> 1 1 <kmeans> <tibble [1 × 4]>

#> 2 2 <kmeans> <tibble [1 × 4]>

#> 3 3 <kmeans> <tibble [1 × 4]>

#>

#> $data$user_item_tbl

#> # A tibble: 12 × 8

#> group_id ts_x_acf1 ts_x_acf10 ts_diff1_acf1 ts_diff1_acf10 ts_diff2_acf1

#> <int> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 1 0.741 1.55 -0.0995 0.474 -0.182

#> 2 2 0.730 1.50 -0.0155 0.654 -0.147

#> 3 3 0.766 1.62 -0.471 0.562 -0.620

#> 4 4 0.715 1.46 -0.253 0.457 -0.555

#> 5 5 0.730 1.48 -0.372 0.417 -0.649

#> 6 6 0.751 1.61 0.122 0.646 0.0506

#> 7 7 0.745 1.58 0.260 0.236 -0.303

#> 8 8 0.761 1.60 0.319 0.419 -0.319

#> 9 9 0.747 1.59 -0.235 0.191 -0.650

#> 10 10 0.732 1.50 -0.0371 0.269 -0.510

#> 11 11 0.746 1.54 -0.310 0.357 -0.556

#> 12 12 0.735 1.51 -0.360 0.294 -0.601

#> # ℹ 2 more variables: ts_seas_acf1 <dbl>, ts_entropy <dbl>

#>

#> $data$cluster_tbl

#> # A tibble: 12 × 9

#> cluster group_id ts_x_acf1 ts_x_acf10 ts_diff1_acf1 ts_diff1_acf10

#> <int> <int> <dbl> <dbl> <dbl> <dbl>

#> 1 2 1 0.741 1.55 -0.0995 0.474

#> 2 2 2 0.730 1.50 -0.0155 0.654

#> 3 1 3 0.766 1.62 -0.471 0.562

#> 4 1 4 0.715 1.46 -0.253 0.457

#> 5 1 5 0.730 1.48 -0.372 0.417

#> 6 2 6 0.751 1.61 0.122 0.646

#> 7 2 7 0.745 1.58 0.260 0.236

#> 8 2 8 0.761 1.60 0.319 0.419

#> 9 1 9 0.747 1.59 -0.235 0.191

#> 10 1 10 0.732 1.50 -0.0371 0.269

#> 11 1 11 0.746 1.54 -0.310 0.357

#> 12 1 12 0.735 1.51 -0.360 0.294

#> # ℹ 3 more variables: ts_diff2_acf1 <dbl>, ts_seas_acf1 <dbl>, ts_entropy <dbl>

#>

#>

#> $kmeans_object

#> $kmeans_object[[1]]

#> K-means clustering with 2 clusters of sizes 7, 5

#>

#> Cluster means:

#> ts_x_acf1 ts_x_acf10 ts_diff1_acf1 ts_diff1_acf10 ts_diff2_acf1 ts_seas_acf1

#> 1 0.7387865 1.528308 -0.2909349 0.3638392 -0.5916245 0.2930543

#> 2 0.7456468 1.568532 0.1172685 0.4858013 -0.1799728 0.2876449

#> ts_entropy

#> 1 0.6438176

#> 2 0.4918321

#>

#> Clustering vector:

#> [1] 2 2 1 1 1 2 2 2 1 1 1 1

#>

#> Within cluster sum of squares by cluster:

#> [1] 0.3660630 0.3704304

#> (between_SS / total_SS = 59.8 %)

#>

#> Available components:

#>

#> [1] "cluster" "centers" "totss" "withinss" "tot.withinss"

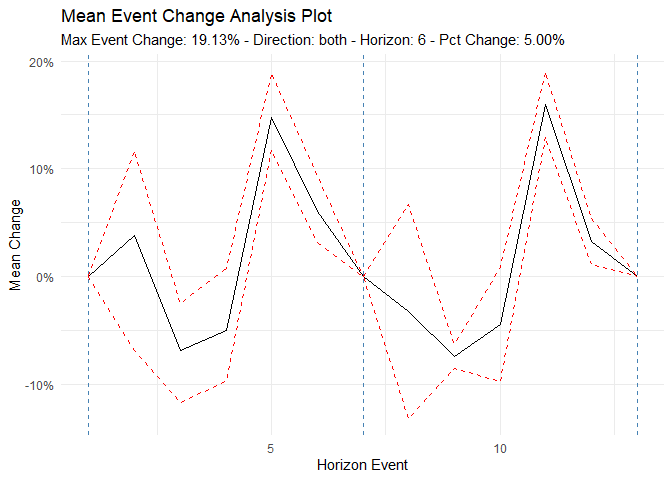

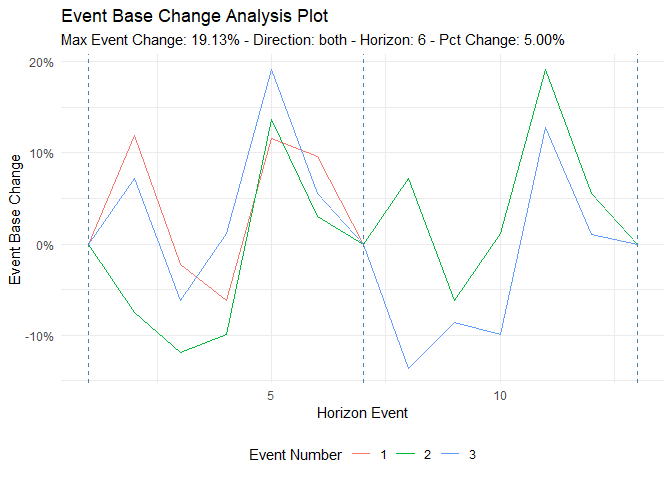

#> [6] "betweenss" "size" "iter" "ifault"Analyze time series behavior before and after significant events (e.g., policy changes, new treatments):

library(dplyr)

df <- ts_to_tbl(AirPassengers) %>% select(-index)

ts_time_event_analysis_tbl(

.data = df,

.horizon = 6,

.date_col = date_col,

.value_col = value,

.direction = "both"

) %>%

ts_event_analysis_plot()

ts_time_event_analysis_tbl(

.data = df,

.horizon = 6,

.date_col = date_col,

.value_col = value,

.direction = "both"

) %>%

ts_event_analysis_plot(.plot_type = "individual")

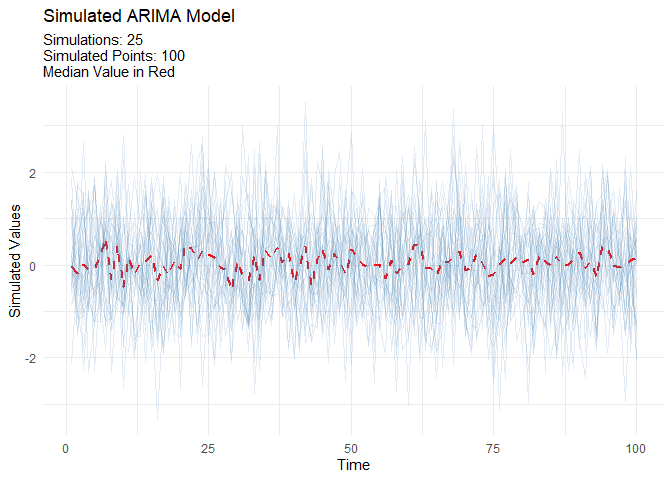

Generate realistic ARIMA time series for testing and validation:

output <- ts_arima_simulator()

output$plots$static_plot

Each function creates a complete modeling pipeline including recipe, model specification, workflow, fitting, and calibration:

| Function | Model Type | Description |

|---|---|---|

ts_auto_arima() |

ARIMA | Automatic ARIMA with auto-tuning |

ts_auto_arima_xgboost() |

Hybrid | ARIMA errors with XGBoost |

ts_auto_prophet_reg() |

Prophet | Facebook’s Prophet algorithm |

ts_auto_prophet_boost() |

Hybrid | Prophet with XGBoost |

ts_auto_xgboost() |

ML | Gradient boosting |

ts_auto_nnetar() |

Neural Net | Neural network autoregression |

ts_auto_exp_smoothing() |

ETS | Exponential smoothing |

ts_auto_smooth_es() |

Smooth | Smooth package ETS |

ts_auto_theta() |

Theta | Theta method |

ts_auto_croston() |

Croston | For intermittent demand |

ts_auto_lm() |

Linear | Linear regression with time features |

ts_auto_mars() |

MARS | Multivariate adaptive regression splines |

ts_auto_glmnet() |

GLM | Elastic net regression |

ts_auto_svm_poly() |

SVM | Support vector machine (polynomial) |

ts_auto_svm_rbf() |

SVM | Support vector machine (radial) |

healthyR.ts includes 90+ functions organized into these

categories:

Contributions are welcome! Here’s how you can help:

Please follow the tidyverse style guide for code contributions.

If you use healthyR.ts in your research or publications,

please cite:

citation("healthyR.ts")Author: Steven P. Sanderson II, MPH

Maintainer: Steven P. Sanderson II, MPH

(spsanderson@gmail.com)

Copyright: © 2020-2025 Steven P. Sanderson II, MPH