![]()

![]()

![]()

This package consists of a series of functions created by the author

(Jacob) to automate otherwise tedious research tasks. At this juncture,

the unifying theme is the more efficient presentation of regression

analyses. There are a number of functions for other programming and

statistical purposes as well. Support for the survey

package’s svyglm objects as well as weighted regressions is

a common theme throughout.

Notice: As of jtools version 2.0.0, all

functions dealing with interactions (e.g., interact_plot(),

sim_slopes(), johnson_neyman()) have been

moved to a new package, aptly named interactions.

For the most stable version, simply install from CRAN.

install.packages("jtools")If you want the latest features and bug fixes then you can download

from Github. To do that you will need to have devtools

installed if you don’t already:

install.packages("devtools")Then install the package from Github.

devtools::install_github("jacob-long/jtools")To see what features are on the roadmap, check the issues section of the repository, especially the “enhancement” tag. Closed issues may be of interest, too, since they may be fixed in the Github version but not yet submitted to CRAN.

Here’s a synopsis of the current functions in the package:

summ())summ() is a replacement for summary() that

provides the user several options for formatting regression summaries.

It supports glm, svyglm, and

merMod objects as input as well. It supports calculation

and reporting of robust standard errors via the sandwich

package.

Basic use:

data(movies)

fit <- lm(metascore ~ budget + us_gross + year, data = movies)

summ(fit)#> MODEL INFO:

#> Observations: 831 (10 missing obs. deleted)

#> Dependent Variable: metascore

#> Type: OLS linear regression

#>

#> MODEL FIT:

#> F(3,827) = 26.23, p = 0.00

#> R² = 0.09

#> Adj. R² = 0.08

#>

#> Standard errors:OLS

#> --------------------------------------------------

#> Est. S.E. t val. p

#> ----------------- ------- -------- -------- ------

#> (Intercept) 52.06 139.67 0.37 0.71

#> budget -0.00 0.00 -5.89 0.00

#> us_gross 0.00 0.00 7.61 0.00

#> year 0.01 0.07 0.08 0.94

#> --------------------------------------------------It has several conveniences, like re-fitting your model with scaled

variables (scale = TRUE). You have the option to leave the

outcome variable in its original scale

(transform.response = TRUE), which is the default for

scaled models. I’m a fan of Andrew Gelman’s 2 SD standardization method,

so you can specify by how many standard deviations you would like to

rescale (n.sd = 2).

You can also get variance inflation factors (VIFs) and partial/semipartial (AKA part) correlations. Partial correlations are only available for OLS models. You may also substitute confidence intervals in place of standard errors and you can choose whether to show p values.

summ(fit, scale = TRUE, vifs = TRUE, part.corr = TRUE, confint = TRUE, pvals = FALSE)#> MODEL INFO:

#> Observations: 831 (10 missing obs. deleted)

#> Dependent Variable: metascore

#> Type: OLS linear regression

#>

#> MODEL FIT:

#> F(3,827) = 26.23, p = 0.00

#> R² = 0.09

#> Adj. R² = 0.08

#>

#> Standard errors:OLS

#> ------------------------------------------------------------------------------

#> Est. 2.5% 97.5% t val. VIF partial.r part.r

#> ----------------- ------- ------- ------- -------- ------ ----------- --------

#> (Intercept) 63.01 61.91 64.11 112.23

#> budget -3.78 -5.05 -2.52 -5.89 1.31 -0.20 -0.20

#> us_gross 5.28 3.92 6.64 7.61 1.52 0.26 0.25

#> year 0.05 -1.18 1.28 0.08 1.24 0.00 0.00

#> ------------------------------------------------------------------------------

#>

#> Continuous predictors are mean-centered and scaled by 1 s.d. The outcome variable remains in its original units.Cluster-robust standard errors:

data("PetersenCL", package = "sandwich")

fit2 <- lm(y ~ x, data = PetersenCL)

summ(fit2, robust = "HC3", cluster = "firm")#> MODEL INFO:

#> Observations: 5000

#> Dependent Variable: y

#> Type: OLS linear regression

#>

#> MODEL FIT:

#> F(1,4998) = 1310.74, p = 0.00

#> R² = 0.21

#> Adj. R² = 0.21

#>

#> Standard errors: Cluster-robust, type = HC3

#> -----------------------------------------------

#> Est. S.E. t val. p

#> ----------------- ------ ------ -------- ------

#> (Intercept) 0.03 0.07 0.44 0.66

#> x 1.03 0.05 20.36 0.00

#> -----------------------------------------------Of course, summ() like summary() is

best-suited for interactive use. When it comes to sharing results with

others, you want sharper output and probably graphics.

jtools has some options for that, too.

export_summs())For tabular output, export_summs() is an interface to

the huxtable package’s huxreg() function that

preserves the niceties of summ(), particularly its

facilities for robust standard errors and standardization. It also

concatenates multiple models into a single table.

fit <- lm(metascore ~ log(budget), data = movies)

fit_b <- lm(metascore ~ log(budget) + log(us_gross), data = movies)

fit_c <- lm(metascore ~ log(budget) + log(us_gross) + runtime, data = movies)

coef_names <- c("Budget" = "log(budget)", "US Gross" = "log(us_gross)",

"Runtime (Hours)" = "runtime", "Constant" = "(Intercept)")

export_summs(fit, fit_b, fit_c, robust = "HC3", coefs = coef_names)| Model 1 | Model 2 | Model 3 | |

|---|---|---|---|

| Budget | -2.43 *** | -5.16 *** | -6.70 *** |

| (0.44) | (0.62) | (0.67) | |

| US Gross | 3.96 *** | 3.85 *** | |

| (0.51) | (0.48) | ||

| Runtime (Hours) | 14.29 *** | ||

| (1.63) | |||

| Constant | 105.29 *** | 81.84 *** | 83.35 *** |

| (7.65) | (8.66) | (8.82) | |

| N | 831 | 831 | 831 |

| R2 | 0.03 | 0.09 | 0.17 |

| Standard errors are heteroskedasticity robust. *** p < 0.001; ** p < 0.01; * p < 0.05. | |||

In RMarkdown documents, using export_summs() and the

chunk option results = 'asis' will give you nice-looking

tables in HTML and PDF output. Using the to.word = TRUE

argument will create a Microsoft Word document with the table in it.

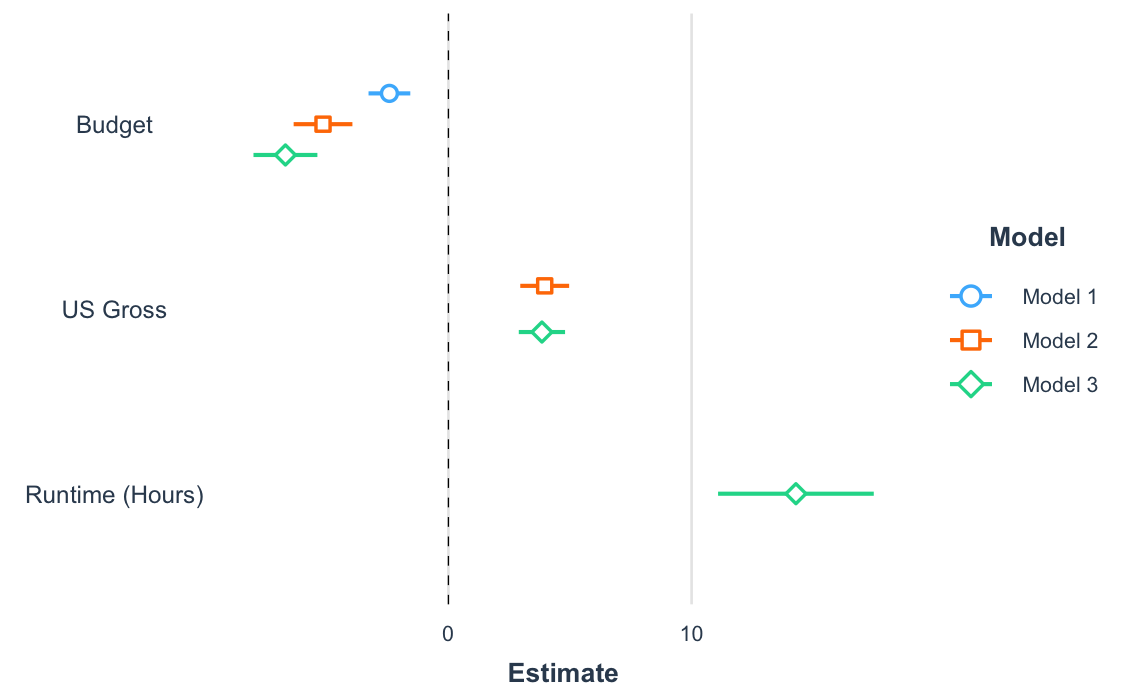

plot_coefs() and

plot_summs())Another way to get a quick gist of your regression analysis is to

plot the values of the coefficients and their corresponding

uncertainties with plot_summs() (or the closely related

plot_coefs()). Like with export_summs(), you

can still get your scaled models and robust standard errors.

coef_names <- coef_names[1:3] # Dropping intercept for plots

plot_summs(fit, fit_b, fit_c, robust = "HC3", coefs = coef_names)

And since you get a ggplot object in return, you can

tweak and theme as you wish.

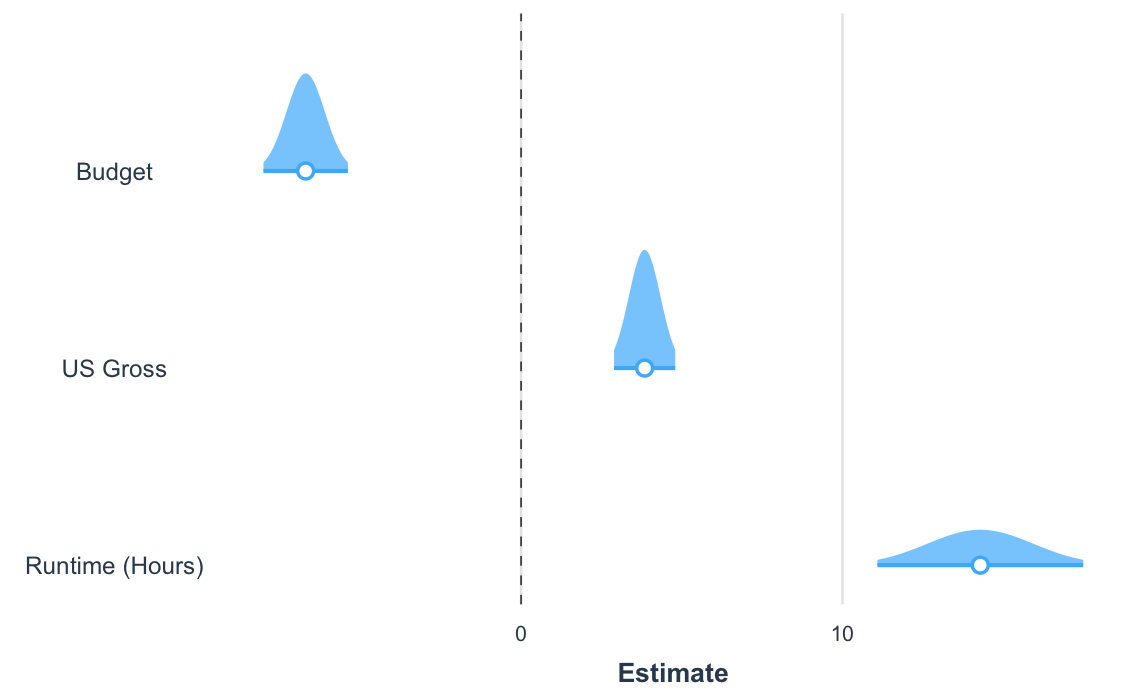

Another way to visualize the uncertainty of your coefficients is via

the plot.distributions argument.

plot_summs(fit_c, robust = "HC3", coefs = coef_names, plot.distributions = TRUE)

These show the 95% interval width of a normal distribution for each estimate.

plot_coefs() works much the same way, but without

support for summ() arguments like robust and

scale. This enables a wider range of models that have

support from the broom package but not for

summ().

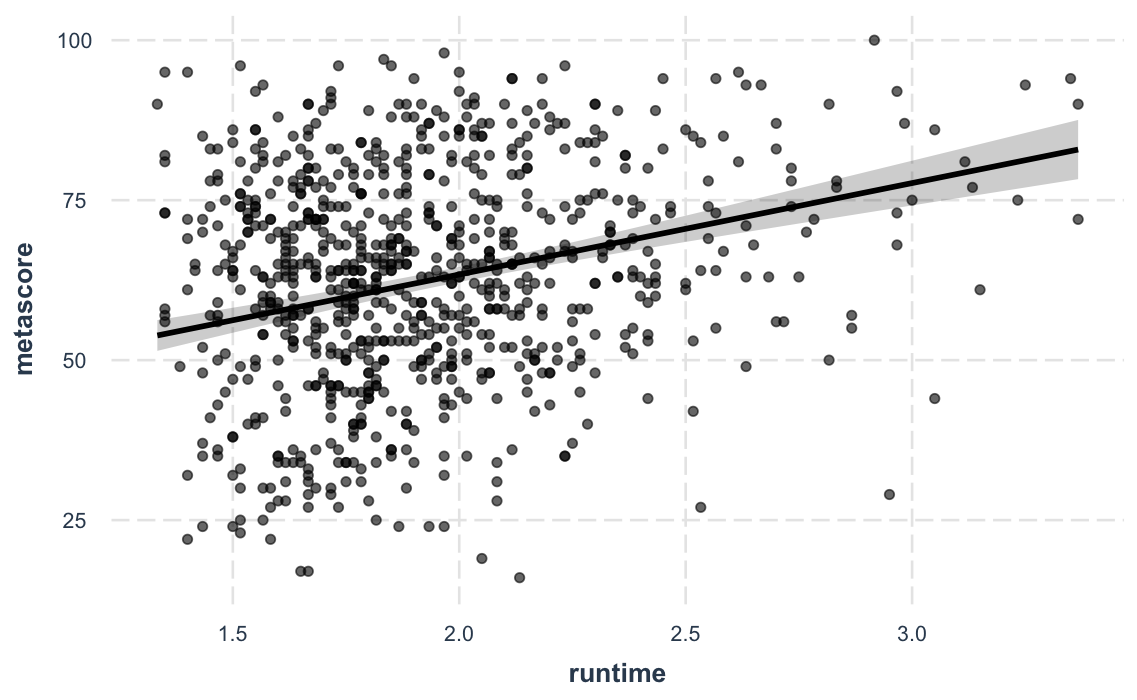

effect_plot())Sometimes the best way to understand your model is to look at the

predictions it generates. Rather than look at coefficients,

effect_plot() lets you plot predictions across values of a

predictor variable alongside the observed data.

effect_plot(fit_c, pred = runtime, interval = TRUE, plot.points = TRUE)#> Using data movies from global environment. This could cause incorrect

#> results if movies has been altered since the model was fit. You can

#> manually provide the data to the "data =" argument.

#> Warning: Removed 10 rows containing missing values or values outside the scale range

#> (`geom_point()`).

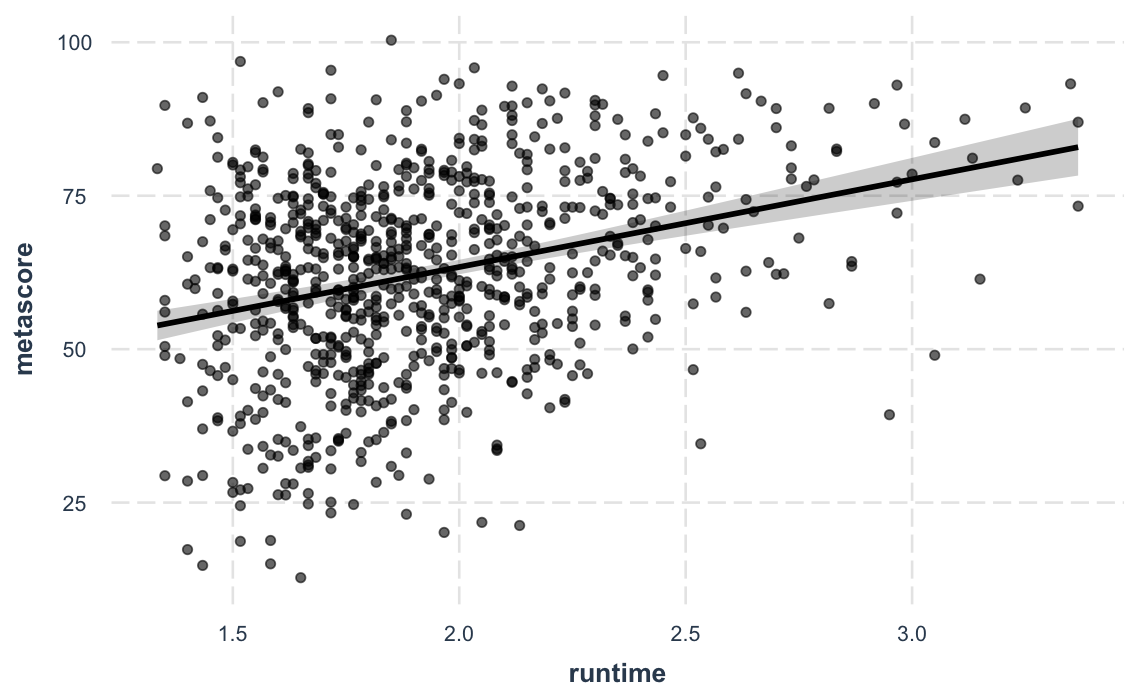

And a new feature in version 2.0.0 lets you plot

partial residuals instead of the raw observed data, allowing

you to assess model quality after accounting for effects of control

variables.

effect_plot(fit_c, pred = runtime, interval = TRUE, partial.residuals = TRUE)#> Using data movies from global environment. This could cause incorrect

#> results if movies has been altered since the model was fit. You can

#> manually provide the data to the "data =" argument.

Categorical predictors, polynomial terms, (G)LM(M)s, weighted data, and much more are supported.

There are several other things that might interest you.

gscale(): Scale and/or mean-center data, including

svydesign objectsscale_mod() and center_mod(): Re-fit

models with scaled and/or mean-centered datawgttest() and pf_sv_test(), which are

combined in weights_tests(): Test the ignorability of

sample weights in regression modelssvycor(): Generate correlation matrices from

svydesign objectstheme_apa(): A mostly APA-compliant

ggplot2 themetheme_nice(): A nice ggplot2 themeadd_gridlines() and drop_gridlines():

ggplot2 theme-changing convenience functionsmake_predictions(): an easy way to generate

hypothetical predicted data from your regression model for plotting or

other purposes.Details on the arguments can be accessed via the R documentation

(?functionname). There are now vignettes documenting just

about everything you can do as well.

I’m happy to receive bug reports, suggestions, questions, and (most of all) contributions to fix problems and add features. I prefer you use the Github issues system over trying to reach out to me in other ways. Pull requests for contributions are encouraged. If you are considering writing up a bug fix or new feature, please check out the contributing guidelines.

Please note that this project is released with a Contributor Code of Conduct. By participating in this project you agree to abide by its terms.

This package is licensed under the GPLv3 license or any later version.